Smart contracts are self-enforcing computer programmes that become more secure on the blockchain. The blockchain is a decentralized and distributed ledger spread across the internet. It allows the storage of information in multiple locations around the world, making it difficult to lose or alter data. In addition, it has rules that govern additions to its content, which makes it difficult to spoof or edit information. The blockchain also provides encryption with public and private keys to enhance privacy and security. As the technology continues to evolve, it is becoming more reliable and trustworthy.

Blockchain and Smart Contracts in Online Dispute Resolution

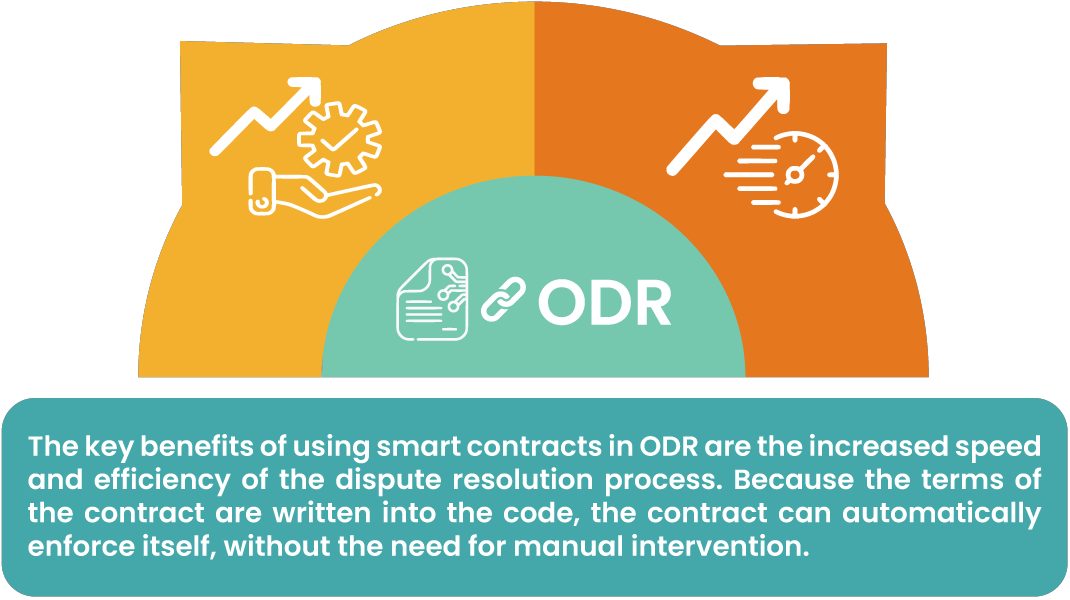

Online Dispute Resolution (ODR) is increasingly using smart contracts to automate the resolution of disputes transparently and efficiently. These can save time and cost in dispute resolutions while increasing the accuracy and consistency of the outcome.

Another benefit of using smart contracts in ODR is the increased transparency and fairness of the process. The terms of the contract are transparent and publicly available. Hence, parties to the dispute can see exactly what they are agreeing to and trust in fair and impartial enforcement. This builds trust and confidence and encourages parties to resolve disputes through ODR instead of traditional forms of dispute resolution.

Despite these benefits, the use of smart contracts in ODR faces challenges. A key challenge is a need for a certain level of technical expertise to understand and use them. This can be a barrier to entry for some parties, particularly those unfamiliar with blockchain technology or coding.

Another challenge is the issue of enforceability. Because many jurisdictions don’t yet recognize smart contracts as legal, it may be difficult to enforce one’s terms in court. This can create uncertainty and may discourage some parties from using smart contracts in ODR.

Case Study I: Kleros Final Award – Mexican Court

Smart Contracts in ODR in India

Indian courts have not heavily tested the notion of blockchain arbitration yet. Historically, Indian courts have taken a relatively suspicious view of arbitration, which has only recently begun to change.

We need to examine two key facets of the applicability of smart contracts in India’s ODR space in detail:

The agreement has to be in writing

According to Section 7 of the Arbitration and Conciliation Act 1996, an arbitration agreement must be “in writing,” but communicating the agreement through “electronic means” also satisfies this requirement. An amendment to the Act in 2015 added this provision, but it does not define the term “electronic means”. A similar provision in the Information Technology Act 2000 defines “electronic means” as a method of creating an “electronic record,” which includes data stored or transmitted electronically. There is a possibility that one could consider blockchain arbitration agreements, which use smart contracts in programming code to execute actions for predetermined conditions, as a form of communication through “electronic means,” but the courts or the Law Commission have not yet definitively answered this question.

Jurisdiction/Territory

India has a reservation to the New York Convention that limits the recognition and enforcement of foreign arbitral awards to certain parties to the Convention. Blockchain arbitration — decentralized by nature — may not meet the requirements for territoriality in India and may therefore not be enforceable. This is because India has not recognized awards made online outside of any particular territory. It is possible that legislation could address this issue, and a report from NITI Aayog in October 2021 suggested that blockchain-based smart contracts could potentially transform arbitral processes.

Indian Landscape and Legal Implications

The use of smart contracts is gaining traction in India, as a way to automate their execution and reduce the need for manual intervention. The Indian government has had a chequered past with blockchain applications, including a ban on virtual currencies in 2018, which the Supreme Court later quashed. The Indian Contract Act, 1872 requires that for a contract to be valid, it must satisfy the criteria of offer, acceptance, and consideration. In the case of smart contracts, the publishing of code on a blockchain would be the equivalent of an offer, while another party’s acceptance of that offer would be their assent to the contract. The performance of the tasks outlined in the code would receive valid consideration. However, Indian law may not recognize smart contracts without digital signatures and authentication in accordance with the Information Technology Act of 2000.

Another legal implication is the issue of liability. In the event of a breach of a smart contract, it may be difficult to determine who is responsible and how to hold them accountable. This is because smart contracts are executed automatically, without the need for manual intervention. This can create uncertainty and may make it difficult to assign responsibility in the event of a breach.

Furthermore, the use of smart contracts may also have implications for existing laws and regulations. For example, they may be subject to different laws and regulations depending on the nature of the contract and the parties involved. This can create complexity and may require careful legal analysis in order to ensure compliance.

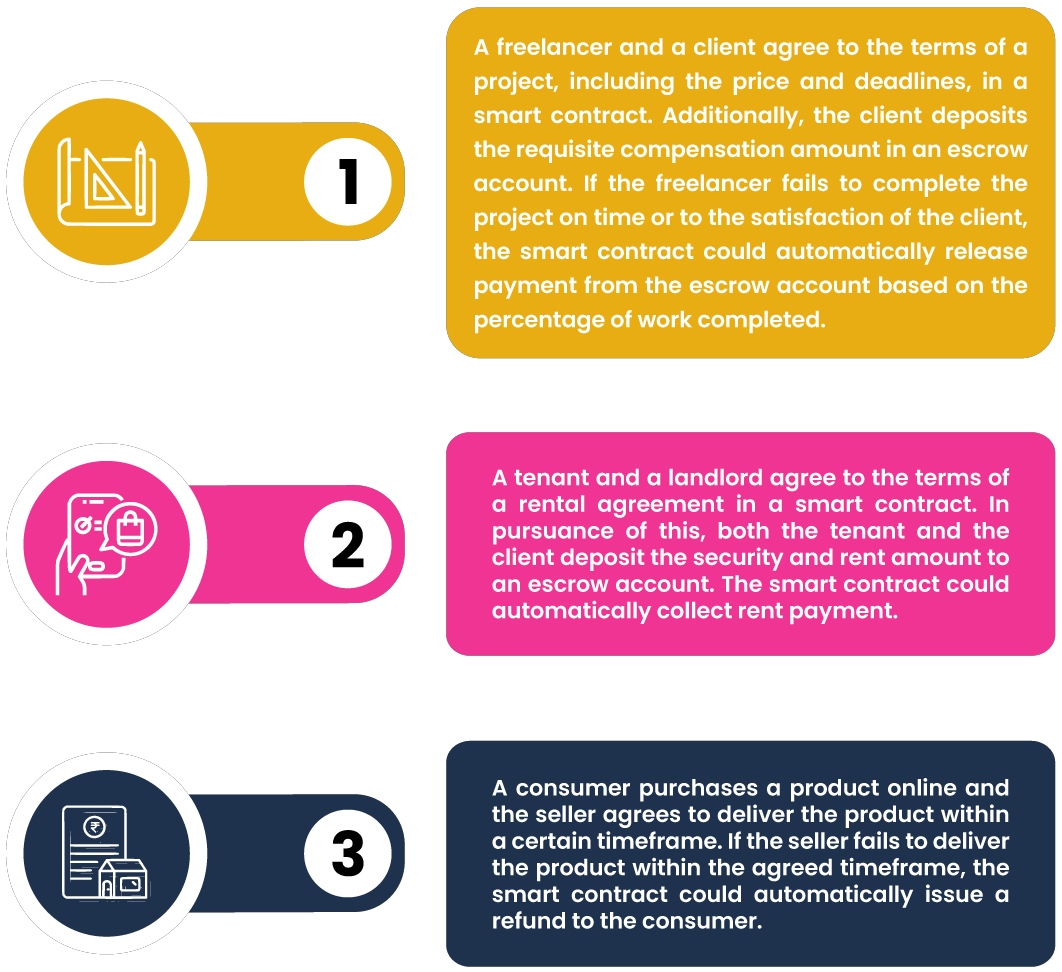

Use-cases

One of the many possible use cases of smart contracts in ODR is to automate the resolution process for disputes that arise in online transactions. Some of the scenarios are illustrated in the figure below:

Conclusion

Overall, the use of smart contracts in India is a rapidly evolving area, and there are many legal implications that need to be considered. Further work is needed to develop a clear legal framework for the use of smart contracts in India, in order to provide clarity and certainty for parties who wish to use them.

Despite the potential benefits of smart contracts, there are a number of regulatory and policy issues that need to be addressed. These include concerns about jurisdiction and the potential for fraud due to the anonymity of the process. In order for smart contracts to be implemented successfully, the Indian regulatory framework would need to be amended and aligned to govern their use.